Case Study: "I Thought My Policy Was Just for My Family After I'm Gone": How One Review Changed Everything

The Opportunity Hidden Inside Existing Policies

Every advisor has clients who bought a life insurance policy years ago, filed it away, and never looked at it again. It's one of the most common, and costly, patterns in the industry. Not because those policies are bad, but because clients rarely understand the full scope of what they own.

This case study follows one such scenario: a 58-year-old business owner, a decade-old whole life policy, and an annual review meeting that unlocked a planning conversation neither the client nor her advisor had fully anticipated.

Background: A Client Who Thought She Was Covered

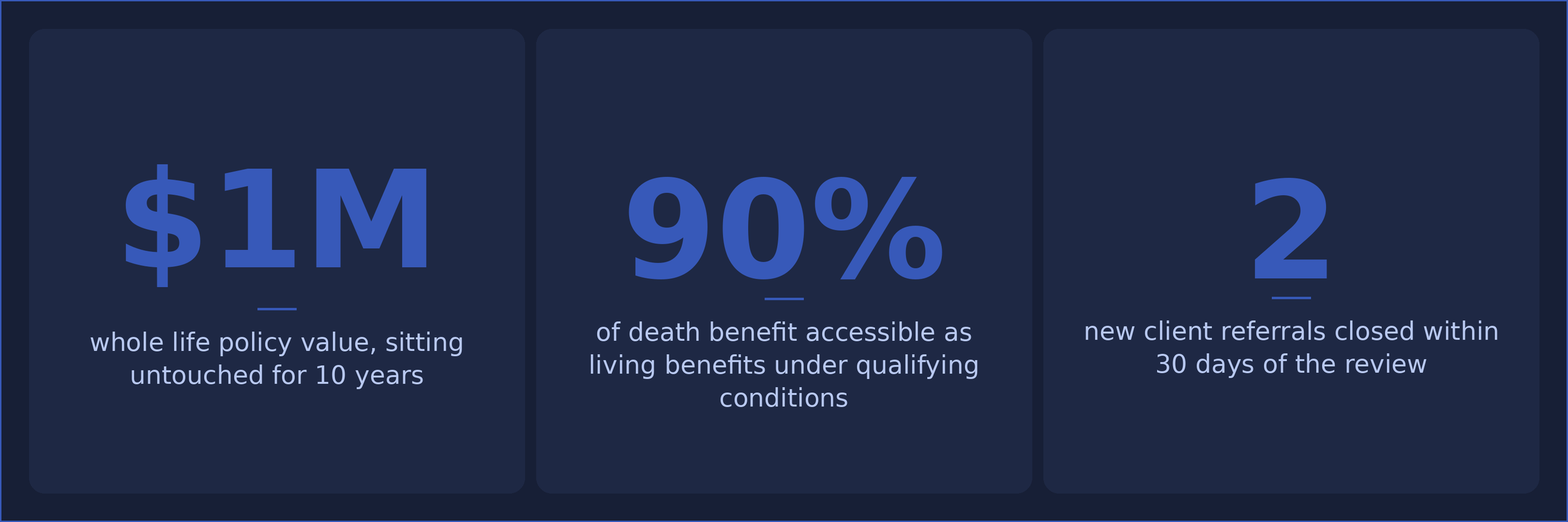

The client, a successful business owner in her late 50s, had purchased a $1 million whole life policy over a decade ago. The original goal was straightforward: income replacement for her family if she passed unexpectedly, with a secondary benefit of building cash value over time.

From her perspective, the policy was doing exactly what she needed. She paid her premiums, the policy grew, and she rarely thought about it. She certainly hadn't revisited it in the years since her business had grown significantly, her personal financial picture had changed, and her long-term care risks had quietly become more relevant.

What she didn't know, and what most policyholders don't know, is that her policy included a chronic illness rider that she had never been told about in plain language.

The Conversation That Changed Everything

Her advisor brought her in for a routine annual review, the kind of meeting that too often becomes a formality. This time, the advisor came prepared to walk through the policy's living benefits for the first time.

The conversation covered three things the client had never fully understood:

1. The Chronic Illness Rider

Her policy included an accelerated death benefit rider triggered by a qualifying chronic illness diagnosis. Under IRS guidelines, she could access up to 90% of her $1 million death benefit tax-free while still living. Funds she could use for care costs, business continuity, or income replacement if she became unable to work.

2. The Long-Term Care Gap

As a business owner without a spouse, the client had no plan for who would manage her business or cover her personal care needs if she experienced a health event. The advisor walked through how a long-term care rider added to her existing policy could create a dedicated funding source for care, without requiring her to purchase a separate standalone policy.

3. The Estate and Beneficiary Update

Her beneficiaries hadn't been reviewed since the policy was issued. Her business had grown, she had brought on two partners, and her estate had become meaningfully more complex. The advisor identified that her current beneficiary designations no longer aligned with her wishes and flagged the need for an updated review with her estate planning attorney.

What Happened Next: From a Routine Review to a Referral Engine

Within 30 days of the review meeting, three meaningful outcomes were documented:

Policy enhancement: The client added a long-term care rider to her existing whole life policy, creating a dual-purpose asset that addressed both her protection needs and her longevity risk, without purchasing an entirely new product.

Beneficiary restructuring: Working alongside her estate planning attorney, her beneficiary designations were updated to reflect her current business structure and personal wishes, with a trust named as the primary beneficiary for the business-owned portion.

Two qualified referrals: When she mentioned the review to two of her closest business peers. Both had similar whole life policies they'd never revisited, and they asked to be connected with her advisor. One new case was closed within 30 days; the second was in active discussion.

Why This Matters for Advisors in 2026

This case isn't unusual. It's the rule, not the exception. According to LIMRA's 2026 research, more than 100 million Americans acknowledge a coverage gap, and growing interest in living benefits and hybrid life + long-term care solutions is reshaping what advisors need to lead with.

The shift happening in 2026 is a fundamental reframing: life insurance is no longer positioned as a "someday" product. It's a living asset, one that provides financial optionality during a client's lifetime, not just a payout at death. Advisors who can articulate this clearly are winning more clients, deeper trust, and more referrals.

The annual review meeting is the single most underutilized business development tool most advisors already have access to. The question isn't whether to have it. It's whether you're walking in prepared to have the right conversation.

Key Takeaways for Advisors

Schedule a dedicated policy review for every client who purchased coverage more than three years ago. Most have never had a living benefits conversation

Lead with the chronic illness rider before discussing standalone LTC. It's often already in the policy and immediately actionable

Use the beneficiary update as a natural bridge to estate planning attorneys and CPAs. It opens the door to the broader advisory team

Referrals follow education: when clients understand what they own, they talk about it, and that conversation is your best prospecting tool

Hybrid life + LTC products are growing fast in 2026; clients who are 50–65 are the primary audience and they're actively looking for stability and simplicity

The Bottom Line

Life insurance has always been built on trust. But in 2026, the advisors who earn that trust aren't just the ones who sell the right product. They're the ones who come back, year after year, and show clients what they already have. The annual review isn't overhead. It's the product.

Ready to Have This Conversation With Your Clients?

Our team can help you prepare for living benefits reviews and identify the right products for your clients' longevity planning needs. Reach out!

This case study is for illustrative and educational purposes only. Client details have been generalized to protect privacy. This content does not constitute financial, legal, or tax advice. Product availability, rider terms, and benefit amounts vary by carrier and policy. Always review specific policy language and consult with appropriate professionals before making recommendations.