The College Funding Tool Most Families Overlook

Graduation season has a way of bringing the cost of college into focus. For the parents and grandparents in your book of business who want to help fund an education, the numbers are sobering, and they keep climbing.

$30,990 per year. Average total cost at an in-state public college.

$65,470 per year. Average total cost at a private college.

Over four years, those figures can stretch past $120,000 at a public school and approach $260,000 at a private one. A savings strategy that starts early can make a meaningful difference. The question for many families is not whether to save, but which tools to use.

Most families know about the 529 plan. Far fewer realize that cash value life insurance can play a supporting role in the same plan. Both deserve a place in the conversation, and understanding how they differ helps your clients make a confident choice.

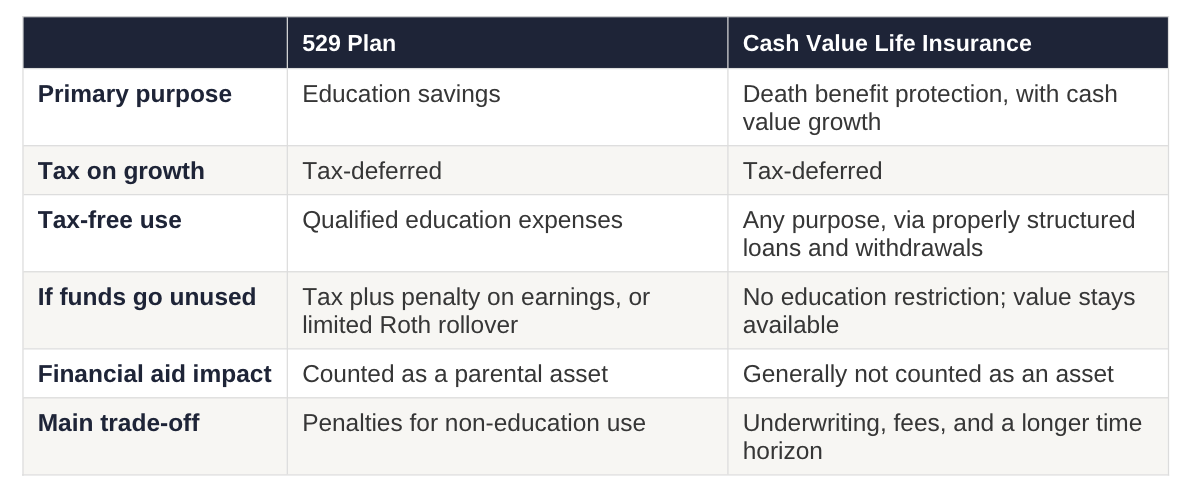

The 529 Plan

A 529 is a dedicated education savings account. Contributions are made with after-tax dollars, earnings grow tax-deferred, and withdrawals are federal income tax-free when used for qualified education expenses such as tuition, fees, books, and room and board. Many states also offer a state tax deduction or credit for contributions.

It is purpose-built for education, which is both its strength and its limitation:

Strong tax treatment when funds are used for qualified education costs.

High contribution ceilings and straightforward setup.

If funds are withdrawn for non-education purposes, the earnings portion is generally subject to income tax plus a 10 percent federal penalty.

Recent rules allow a limited lifetime amount, currently up to $35,000, to be rolled into the beneficiary’s Roth IRA when conditions are met, which softens the “what if it goes unused” concern.

A parent-owned 529 is treated as a parental asset on the FAFSA, generally assessed at a maximum of 5.64 percent, so its impact on need-based aid is relatively modest.

Cash Value Life Insurance

Permanent life insurance, including indexed universal life (IUL), is designed first to provide a death benefit. Alongside that protection, a portion of the premium builds cash value that grows tax-deferred. With IUL, that growth is tied to a market index with a floor that limits downside and a cap that limits the upside.

Because the policy is not tied to education by definition, the accumulated value can be accessed for any purpose, including tuition, through withdrawals and policy loans that are generally income tax-free when the policy is structured and maintained properly. A few points worth highlighting for clients:

Tax-deferred growth, with the potential for tax-advantaged access to cash value during life.

Funds are not restricted to education, so unused money can support a first home, a business, or retirement.

The cash value of a life insurance policy is generally not reported as an asset on the FAFSA, so it typically does not count against need-based aid.

The death benefit provides protection for the family while the cash value accumulates.

It requires medical underwriting, carries insurance costs and fees, and works best as a long-term commitment. It is not a fit for short time horizons.

Side by Side

A Quick Example

Consider a couple in their late 30s with a newborn and a second child on the way. They want to help with college, but they are equally worried about protecting their family’s income while the kids are young.

A 529 plan gives them a focused, tax-advantaged way to save specifically for school. Layering in a properly funded cash value policy adds a death benefit that protects the household today, builds value they can tap for tuition later, and stays flexible if one child earns a scholarship or chooses a different path. Used together, the two tools cover more ground than either one alone.

When Both Make Sense

For many families, this is not an either-or decision. A 529 plan can do the heavy lifting on dedicated education savings, while cash value life insurance adds protection, flexibility, and a backstop for the money that does not get used. The right balance depends on the family’s income, time horizon, aid expectations, and how much certainty they want around the death benefit.

That is where your guidance matters most. Helping clients see the full picture, rather than defaulting to a single account, is what turns a savings habit into a strategy.

Let’s build the right plan together. Watermark Life can help you model both options for your clients and find the combination that fits. Connect with us!

Source: College Board, Trends in College Pricing and Student Aid 2025. Cost figures reflect average total cost of attendance, including tuition, fees, housing, food, and other expenses.

This information is educational only and is not intended as tax, legal, or investment advice. Watermark Life does not provide tax advice. Guarantees are based on the claims-paying ability of the issuing insurer. Policy loans and withdrawals reduce the cash value and death benefit and may have tax consequences if the policy lapses or is surrendered. Tax rules and financial aid formulas are subject to change. Clients should consult a qualified tax, legal, or financial professional regarding their individual circumstances.